While investors, newspapers and political leaders are fretting about the war in the Middle East, some things are taking place that very few people are closely paying attention to. We have warned about this war and other wars that are coming. This war puts a huge cost on Europe and China, and the war can still escalate. Although this war has the potential to devastate Europe .. it so far a “managed war” – managed in the sense that you are being told what you are allowed to do and what you are not allowed to do (for instance bombing strategic installations). But total wars are coming .. and they will resemble WW2.

Much of what is being overlooked cannot be connected and linked together unless you understand the extent of the macroeconomic trap Western economies are in. Western leaders have reached a point of no return over the past 2 months. It is the level of national Debt versus GDP that is actually increasingly driving monetary policy, fiscal policy, foreign policy and geopolitics.

Some people keep looking for more commentary on that which is already saturating the newsreels. To survive and thrive in this decade, we need to focus on that which the masses are not paying attention to. Although I could write seven-eight pages about the current war in the Middle East, I will not expand on it. Few people can withstand the temptation to repeat what is public domain already and to add their every comment on current affairs. But honestly, there is little we could add, that we have not discussed or predicted already or that you have not read elsewhere. We would only be breaking our editorial policy.

Since 2017 we are expecting three large scale wars in the Middle East. And in one of those wars (potentially two) weapons of mass destruction will unfortunately be deployed. We didn’t expect three managed wars in the Middle East, they are likely to be all out wars.

Debt and geopolitics

Our message today: Debt to GDP ratios are increasingly driving Foreign Policy and Geopolitics. Just as people across the West fret about the Middle East war .. their paper money is being debased, they are being taxed again, governments have set eyes on their pensions and the doors to exit are being closed. And no major TV station or important newspaper is showing the full scale of it all. In fact it is piecemeal news at the margin. People are being “bombarded” about events they can do nothing about instead.

To organise a back up base or to diversify your assets in the Southern hemisphere takes years – Those who haven’t started the process are probably pretty much stuck in the Northern hemisphere now. By now people realise that quitting your homebase to embrace a tax haven with glamorous lifestyle and safe streets is not enough … as Dubai exemplifies these days. Many British and Swiss bankers that sent their clients there overlooked the most important factor of this decade: the geopolitical risks.

Crises are welcome

Back in 2022 a journalist asked me why I was so confident the war in Ukraine would not be settled any time soon. “Too many governments will benefit from this war” I told him. The reason why so many people were surprised at my answer was their perspective. They said “Christian, we simply can’t afford this war”. They thought and still think that all governments want to cut costs, balance their budgets and restore stability.

They overlook one important detail – where we are in the cycle. You see – Once you are hopelessly indebted, some more debt and bigger deficits doesn’t matter actually. Especially if your peers are moving in tandem. Why? Rather than saying “we won’t pay you”, you have begun to use Financial Repression to water down your citizens’ wealth and income in order to reduce the real burden of your debt. Take it a step further – You may be even happy about a big shock (even better an external threat) that allows you to use extraordinary executive powers, galvanises national unity and paves the way for higher taxes. In such an environment any opposition will struggle to take power. This is especially true in Europe, where the state owns or dominates mainstream media and there are large pools of private savings in the system.

Looking at Europe – No matter how we got into a crisis, it is not going to be easy to get out of it. While the fiscally healthy nations of South East Asia and Latin America try to restore stability as soon as possible, the highly indebted Western economies have currently few incentives to end the crises – while some are trapped, others are even thriving in it. Some people use conspiracy theories to explain what is unfolding in some key Western economies, but often it is the simple math of economic incentives confined by our political process and legal framework that is at work. As a trained economist I don’t assume evil intent if a monetary incentive or political expedience explain the same. While that helps us protect a minimum level of trust in society and give some authorities the benefit of the doubt, it allows us to advance our analysis without having to pass judgement. The bottom line for some of our troubled governments is that instead of being voted out of government for their shortcomings or mistakes … their overspending, massive debt and tax-increasing stance can be extended.

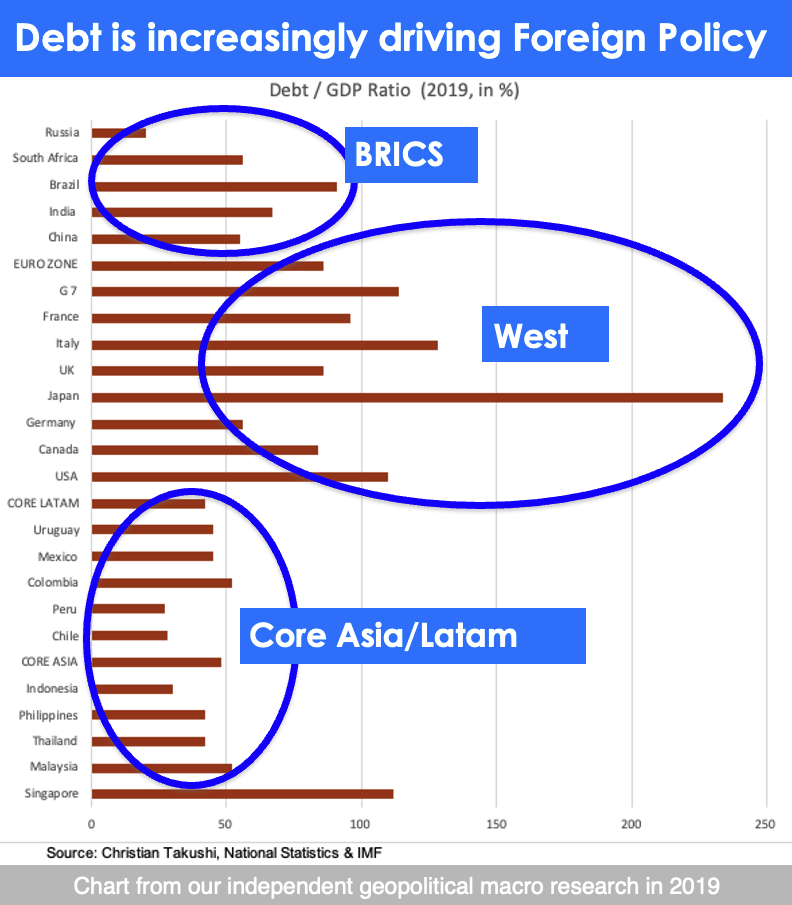

The massive debt load of Western governments is not only increasingly shaping their policy decisions, it is making their actions pretty predictable for their foes and top competitors. Because of COVID effects and recent efforts to manage figures, we prefer to rely in pre-COVID numbers. The numbers from 2019 best reflect the debt levels of leading Western economies, the BRICS and healthy Emerging Markets (three groups that are competing for the future economic rent). The differences in the debt loads are simply huge. The figures for key G7 economies are actually underrepresenting the extent of the debt levels. Our current conservative estimate for G7 debt/GDP is 144%. That is a staggering level. If you understand this debt & deficit complex, you understand that we can’t solve this problem and why I have been telling people to diversify their assets away from Europe, North America and the G20.

The convergence of this with other demographic and geopolitical tendencies across the Northern hemisphere led us in 2015 to expect conflicts, wars, energy & food crises and governments being forced to tax private households with impunity. We said an exodus is coming and eleven years later we see it unfold. At the heart of these diverse trends is one common feature: spiralling debt that is being increasingly underreported. Not so much in emerging markets, but in so-called advanced economies.

Those that know the extent of our true debt levels have a much better understanding of our Foreign Policies. Interestingly, normally geopolitics and economics influence each other. In recent years experts said geopolitics drives policy. That is true on the surface, but behind the scenes, economics is increasingly driving foreign policy in ways few understand. As you read about wars, scandals, conflicts .. pay attention to the debt levels of your economy. Unsustainable debt can be hidden from the academic mind that tends to rely on official data, but it can be spotted by every down-to-earth farmer or housewife. There is no perfect paradise on earth to hide in this age, but the chart below points to economies that have economic incentives to avoid both war and massive taxation.

This research report has been truncated here. If you wish to read the full report or subscribe, you can write to info@geopoliticalresearch.com

Tapping private assets

Discern the signs of the times

Think global

Beware of zero tax havens

Don’t try hiding away in the cyber age

Wealthy and worried

Personal words

When I was eight years old my Japanese father told me “Change can come suddenly, so don’t get too attached to material things – Cherish education, skills and that which you can hold in your heart”. Because his parents survived WW2, he taught me to test everything, think ahead and discern what people are missing out. Without his coaching I would not love complexity today nor would I keep distance to consensus. It is our turn now to train our children for what lies ahead. That might be as important as optimising the strategic asset allocation of your wealth.

Geopolitical Research Team – 17 Mar 2026 (Public release on 20 March 2026 truncated)

info@geopoliticalresearch.com

Geopolitical and economic conditions need close monitoring, because they can change suddenly.

No part of this report should be taken or construed as an investment recommendation.

Since 2016 our newsletter is ranked among the 50 most reliable sources of geopolitical analysis worldwide.

Independent research and releasing a report only when we deviate from consensus adds value.